Longacres Finance

Dividend Yield Theory Explained: A Simple Way to Value Dividend Stocks

Dividend Yield Theory (DYT) is a simple valuation method that compares a stock’s current dividend yield to its historical average. When yield rises above its norm, a stock may be undervalued; when it falls below, it may be overvalued, helping investors time quality dividend buys.

Valuing stocks is one of the hardest parts of investing.

Many investors rely on complicated valuation models, analyst forecasts, or technical indicators that often create more confusion than clarity.

But dividend growth investors have a simpler method that has stood the test of time:

Dividend Yield Theory.

Dividend Yield Theory, often shortened to DYT, is a valuation method that compares a stock’s current dividend yield to its historical average yield.

The idea is simple:

When a high-quality dividend stock yields significantly more than normal, it may be undervalued.

When it yields significantly less than normal, it may be overvalued.

For long-term dividend investors, Dividend Yield Theory can be an incredibly useful tool for identifying attractive buying opportunities while avoiding overpaying for great companies.

Let’s break down exactly how Dividend Yield Theory works and why so many dividend growth investors use it.

What Is Dividend Yield Theory?

Dividend Yield Theory is based on the principle of mean reversion.

Over long periods of time, many mature dividend-paying companies tend to trade within a relatively consistent dividend yield range.

That’s because dividend growth and stock price growth often move together over time.

When stock prices rise much faster than dividends, the yield falls.

When stock prices fall while dividends remain stable or continue growing, the yield rises.

Dividend Yield Theory assumes that eventually the stock’s yield tends to move back toward its historical average.

This creates a simple framework for estimating valuation.

How Dividend Yield Theory Works

The formula itself is extremely simple.

First, determine a company’s:

- Current dividend yield

- Historical average dividend yield

Then compare the two.

If the current yield is higher than the historical average yield, the stock may be undervalued.

If the current yield is lower than the historical average yield, the stock may be overvalued.

For example:

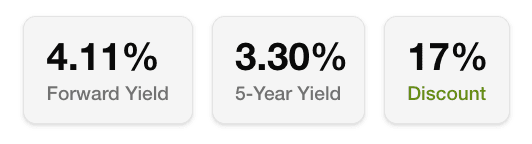

Imagine a company historically yields around 3.3%.

Today, the stock yields 4.11%.

That could indicate the stock price has fallen below fair value relative to its dividend.

On the other hand, if the stock normally yields 3.3% but currently yields only 2.5%, the stock may be trading at an expensive valuation.

Why Dividend Yield Theory Makes Sense

Dividend Yield Theory works best with mature, stable companies that consistently grow their dividends over long periods of time.

These companies often have:

- Predictable cash flow

- Stable payout ratios

- Strong competitive advantages

- Long dividend growth histories

Because their businesses are relatively stable, valuation ranges also tend to remain somewhat stable over time.

In many ways, the dividend yield acts like a valuation anchor.

When investor enthusiasm pushes prices too high, yields compress.

When fear drives prices lower, yields expand.

Dividend Yield Theory helps investors recognize those shifts.

An Example of Dividend Yield Theory

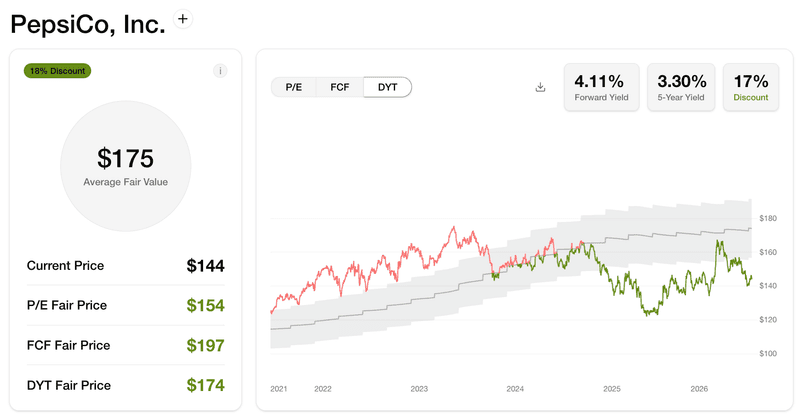

Let’s say a company pays an annual dividend of $5.92 per share.

Historically, the stock has averaged a 3.3% dividend yield.

Using Dividend Yield Theory, we can estimate fair value:

Fair Value Formula

Fair Value = Annual Dividend / Historical Average Yield

In this example:

Fair Value = 5.92 / 0.033 = 179

That suggests the stock’s estimated fair value is approximately $179 per share.

Now imagine the stock is currently trading at $145.

Its yield would rise to 4.1%.

That higher yield may indicate the stock is undervalued relative to its historical norm.

Conversely, if the stock traded at $235, the yield would fall to roughly 2.5%, potentially signaling overvaluation.

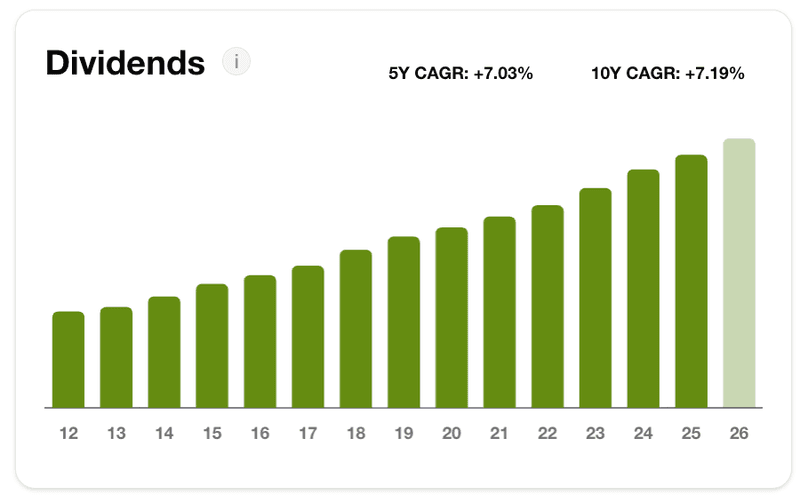

At Yieldr, we take Dividend Yield Theory beyond a single fair value estimate. By combining a company's dividend history with its historical yield, we reconstruct a dynamic Fair Value chart and compare it directly to the stock's actual market price.

This allows you to see not only whether a company appears undervalued or overvalued today, but also how its valuation has evolved over the past five years, providing valuable context that a single point-in-time snapshot simply can't capture.

The Biggest Advantage of Dividend Yield Theory

The biggest advantage of Dividend Yield Theory is simplicity.

Most investors overcomplicate valuation.

Dividend Yield Theory strips away much of the noise and focuses on a single powerful relationship:

Dividend yield relative to historical norms.

This helps investors:

- Avoid chasing overvalued stocks

- Buy quality companies during periods of fear

- Build discipline into the investment process

- Focus on long-term fundamentals instead of short-term price action

For dividend growth investors, this framework can be incredibly valuable during volatile markets.

Dividend Yield Theory Works Best With Certain Types of Stocks

Not every stock is suitable for Dividend Yield Theory.

The strategy works best with companies that have:

- Long dividend histories

- Stable business models

- Consistent dividend growth

- Reliable cash flow

- Reasonable payout ratios

Examples may include:

- Consumer staples companies

- Utilities

- Healthcare companies

- Industrials

- Dividend Aristocrats

The strategy tends to work poorly with:

- Non-dividend paying companies

- Highly cyclical businesses

- Commodity companies

- Companies with inconsistent dividends

- Fast-growing technology stocks

A company with unstable earnings or irregular dividends may not maintain a consistent yield range over time.

Dividend Yield Theory Is Not Perfect

Like every valuation method, Dividend Yield Theory has limitations.

A stock is not automatically undervalued simply because the yield is high.

Sometimes yields rise because the business itself is deteriorating.

This is known as a dividend trap.

For example:

- Earnings may be declining

- Debt levels may be increasing

- The dividend may be unsustainable

- The company’s competitive position may be weakening

That’s why Dividend Yield Theory should never be used in isolation.

Investors should also analyze:

- Revenue growth

- Earnings growth

- Free cash flow

- Payout ratios

- Debt levels

- Return on capital

- Competitive advantages

Valuation matters, but business quality matters even more.

Dividend Yield Theory and Long-Term Returns

One reason Dividend Yield Theory is so powerful is because valuation has a major impact on long-term returns.

When investors overpay for stocks, future returns tend to suffer.

When investors buy high-quality companies at attractive valuations, future returns often improve.

Long-term returns generally come from three sources:

- Earnings growth

- Dividends

- Changes in valuation

Dividend Yield Theory helps investors improve the third component.

Buying undervalued dividend growth stocks can create an additional tailwind as valuations eventually normalize over time.

Why Dividend Growth Investors Love Dividend Yield Theory

Dividend growth investors are naturally focused on cash flow and long-term income growth.

Dividend Yield Theory aligns perfectly with this mindset because it emphasizes:

- Patience

- Valuation discipline

- Long-term thinking

- High-quality companies

Rather than chasing whatever stock is currently popular, Dividend Yield Theory encourages investors to buy quality companies when they become temporarily unpopular.

That mindset is often where the best long-term opportunities are found.

Final Thoughts

Dividend Yield Theory is one of the simplest and most effective valuation tools available to dividend growth investors.

It won’t perfectly predict future stock prices.

No valuation model can.

But it provides a practical framework for identifying when high-quality dividend stocks may be trading above or below fair value.

Most importantly, Dividend Yield Theory helps investors stay disciplined.

Successful investing is not about predicting short-term market movements.

It’s about consistently buying high-quality businesses at reasonable valuations and allowing compounding to work over long periods of time.

Dividend Yield Theory can help investors do exactly that.