Longacres Finance

The Power of Dividends and Compounding

Dividends and reinvestment have driven the majority of long term S&P 500 returns. This article explores the power of compounding, why dividend growth matters more than high yields, and what history teaches about building wealth through quality businesses.

Dividends are often treated as boring.

In a market obsessed with explosive growth, AI, and the next 10x stock, dividends can feel outdated, almost irrelevant.

But history tells a very different story.

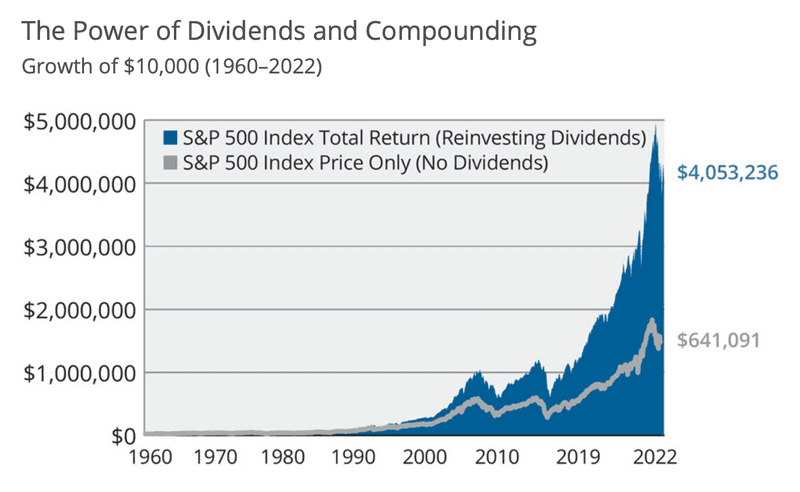

From 1960 through 2022, roughly 69% of the S&P 500’s total return came from dividends and the power of reinvestment. That number alone should completely change how investors think about long term wealth creation.

To put this into perspective:

A $10,000 investment in the S&P 500 without reinvesting dividends would have grown to roughly $641,000.

With dividends reinvested, that same investment would have compounded into more than $4 million.

That is the difference between price appreciation and true compounding.

And importantly, the real magic was not simply receiving dividends, it was reinvesting them consistently over decades.

Dividends Matter Most When Markets Don’t

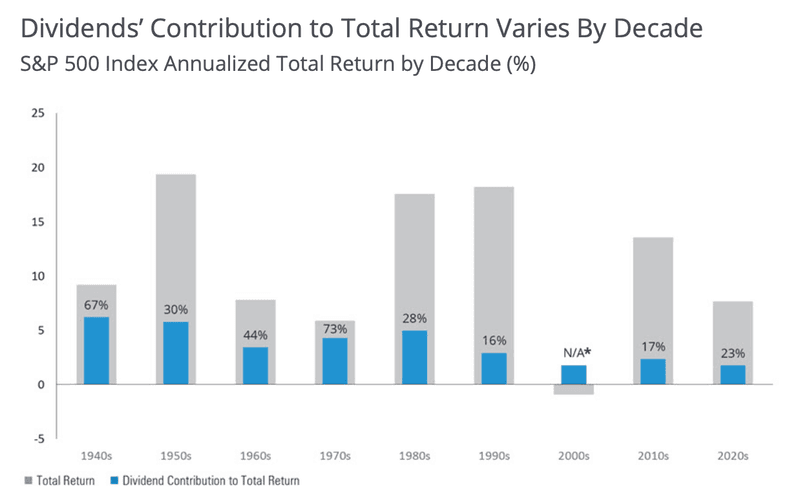

One of the most overlooked aspects of dividends is that their importance changes depending on the market environment.

During periods of explosive market returns, dividends tend to play a smaller role in overall performance. But during slower decades, when capital appreciation becomes harder to find, dividends become a much larger driver of total return.

In other words:

When markets struggle, dividends matter more.

That makes them particularly valuable during prolonged periods of volatility, stagnation, or economic uncertainty.

The Yield Landscape Has Changed Dramatically

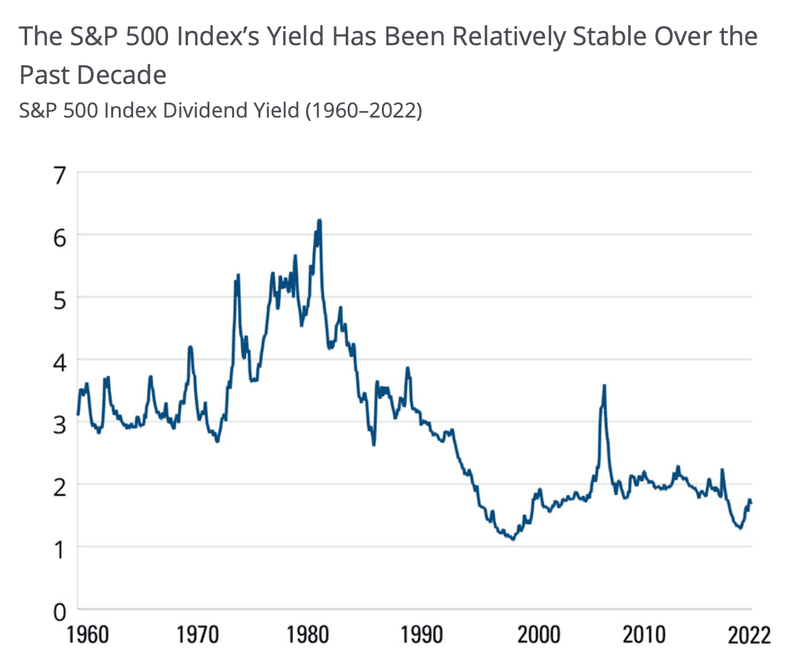

Dividend yields today look very different than they did several decades ago.

During the 1960s, the S&P 500 regularly yielded between 3% and 4%. By the early 1980s, yields briefly climbed above 6%.

Then came the 1990s.

As growth stocks and technology companies dominated the market, dividend yields steadily collapsed. Just before the dot com bubble burst, the S&P 500 yield fell close to 1%.

After the crash, yields recovered as valuations normalized and investors rediscovered the value of cash generating businesses. During the Financial Crisis, the S&P 500 yield climbed back toward 3.5%.

Since then, yields have generally stabilized around 2%, well below historical norms but still meaningful over long periods of compounding.

The era of ultra high index yields may be gone, but dividends continue to serve an important role: they provide tangible returns even when market sentiment deteriorates.

The Problem With Chasing Yield

Many dividend investors naturally gravitate toward the highest yielding stocks.

The logic seems straightforward: Higher yield equals more income equals faster compounding.

But historically, chasing the absolute highest yields has often led investors into weaker businesses, unsustainable payout ratios, and dividend cuts.

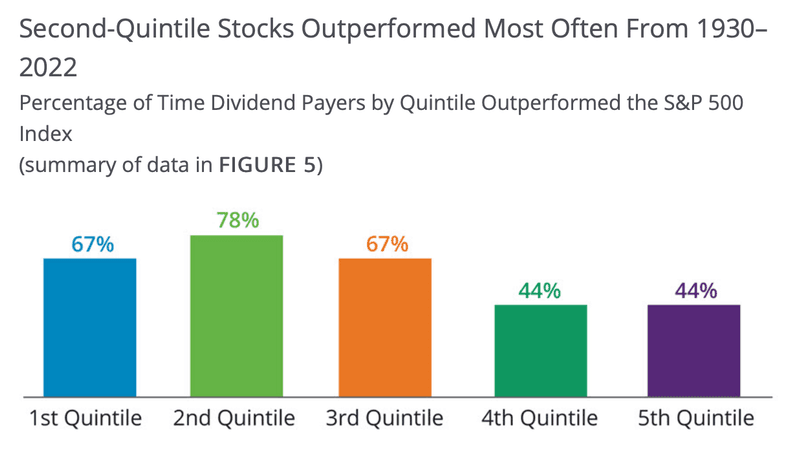

Research from Wellington Management found that the best performing dividend stocks were not the highest yielders, but the second highest yielding group.

These stocks outperformed the broader market 78% of the time.

Why?

Because they struck a healthier balance between:

- attractive income,

- sustainable payout ratios,

- and long term business quality.

The highest yielding group had an average payout ratio near 74%, while the second quintile maintained a far healthier 40% payout ratio.

That difference matters.

An extremely high yield is often a warning sign, not a free lunch.

Dividend Growth Is What Really Matters

The strongest long term results have historically come from companies that consistently grow their dividends over time.

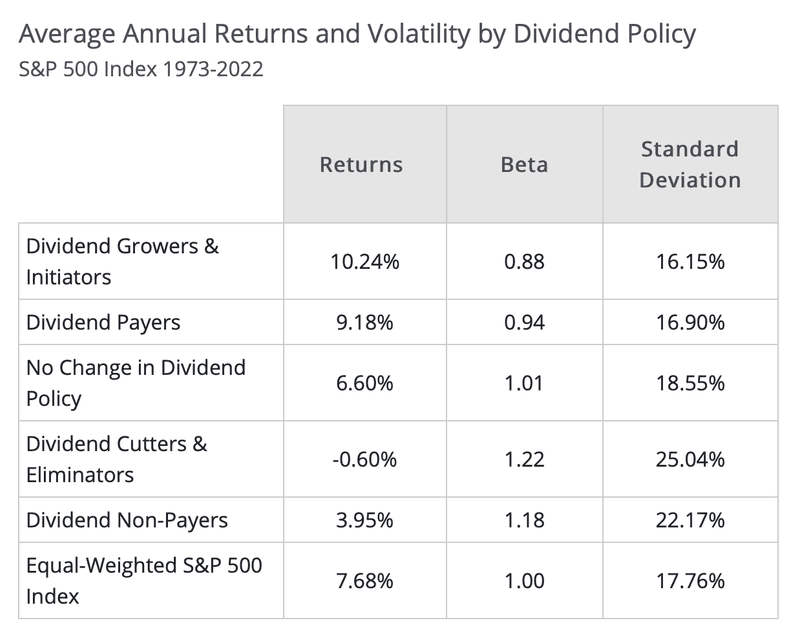

A study from Ned Davis Research analyzed dividend paying stocks between 1973 and 2022 by separating them into groups:

- dividend growers and initiators,

- companies with no dividend policy changes,

- and dividend cutters or eliminators.

The results were remarkably clear.

Dividend growers and initiators delivered:

- the highest returns,

- lower volatility,

- and stronger risk adjusted performance.

Even broad groups of dividend payers outperformed companies that did not pay dividends at all.

Meanwhile, companies that cut or eliminated dividends produced the weakest results overall.

That outcome makes intuitive sense.

Companies capable of consistently increasing dividends are often:

- highly profitable,

- financially stable,

- disciplined allocators of capital,

- and supported by durable cash flows.

Dividend growth is frequently a signal of underlying business strength.

The Bigger Lesson

This does not mean every investor needs to become a dividend investor.

And it certainly does not mean investors should blindly chase yield.

The real lesson is much broader:

Quality matters.

The companies most capable of paying and growing dividends over long periods are often the same businesses with:

- strong balance sheets,

- resilient cash flows,

- durable competitive advantages,

- and disciplined management teams.

Whether you prefer dividend stocks, growth stocks, or broad index funds, the foundation of successful long term investing remains remarkably consistent:

Focus on high quality businesses.

Because over time, compounding works best when supported by durable fundamentals.

The data and charts referenced in this article are based on research published by Hartford Funds.